During the Christmas and New Year holiday period I looked around to see how my current mortgage compared with other products around the place.

I find I do this necessary chore about every other year. In fact, come to think of it throughout our near 9 years here in our humble home we’ve refinanced 3 times, which includes the recent one we’re in the throes of doing (more on that throughout this article), with our last refinancing happening around April 2018.

Unfortunately not all refinancing deals have been as good as I would have liked, so in this article I want to impart what I’ve learnt so that you don’t make the same mistakes I have.

Trap #1 – Refinancing for 30 Years (Again!)

I’ve made this mistake every time (except with our new financier).

This means you never really get to throw good chunks of principal at your home loan to reduce it down. By starting at 30 years again you just end up paying the new financiers more in interest – which is why you need to be vigilant when you move.

Most refinancing calculators and applications will default your home loan to 30 years, be wary of this and make sure you change it when you speak to someone on the phone.

Sadly most lenders will put the onus on you to make extra repayments, but we all know that while this sounds good it invariably never happens.

Therefore, if you can’t get your home loan term set to anything less than 30 years – don’t proceed. Find another financier who would be willing to work with you, not against you.

Interestingly when I started looking around for cheaper deals on home loans, one such financier was getting “Editors Choice” awards from several different web sites.

The lender was Ubank Home Loans .

Ubank was already familiar to my wife and I as back in 2010 when we were newlyweds we started saving for our house. As the months wore on in our hunting we found the area we liked and got everything ready to pull the trigger. This meant when our cash term deposit at ANZ was up we moved it to a more accessible and high interest bearing account by moving our house deposit to Ubank.

While we weren’t with Ubank for too long we were impressed with the ease of use and the accessibility. And that was 10 years ago.

Since then we bought our house and withdrew everything (except for 1 cent in interest which is still holding the fort).

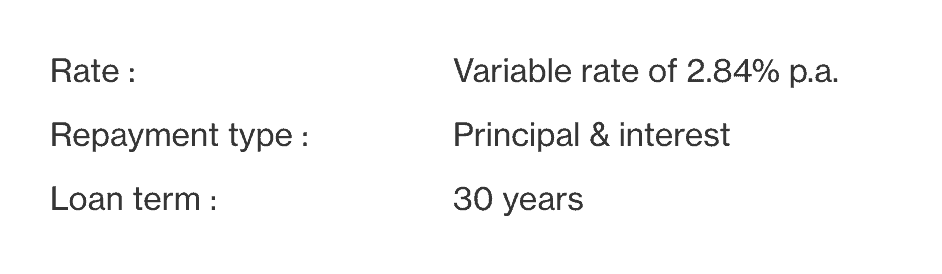

So when I went through Ubank’s home loan application process where they offered us a nice cool 2.84%pa principal & interest rate – I didn’t hesitate.

Roadblocks with Ubank’s Home Loan Application Process

While the initial parts of Ubank’s home loan form were easy to proceed through there were a couple of roadblocks I hit, the main one being:

Home Loan Term defaulted to 30 years and there was no clear way where this could be changed.

Ugh .

(The another minor gripe was inputting my monthly living expenses. This would take time for every applicant and would be so much easier if Ubank was given authority to connect to my current bank and do its analysis on our spending.)

Anyway, the point to make here is to not re-settle with a 30 year term on a home loan you’re refinancing. If you’re ever struggling with what term to use, either use the current term on your existing mortgage or use the length of years you’ve been in your house minus 30 years.

Trap #2 – Increasing Your Home Loan Amount

While you might keep the same mortgage term it’s just as important to keep the same amount (or less) than your current home loan balance.

I made the mistake of refinancing a larger amount than my existing mortgage as I thought I would need the extra money for renovations or a car or something just as stupid.

That was silly.

Not only was I paying a larger portion of interest with each repayment because I had refinanced to 30 years, but I also increased my principal amount!

What made this deal even worse was that I redrew the full amount and the new loan didn’t have any offset facility, meaning the extra amount I had in principal that I wasn’t using wasn’t even reducing the interest!

Now if I want to buy a new car or perform a reno I just use all my superpowers to save up and buy it outright with cash. There shouldn’t be a need to redraw on my home loan or to increase my home loan principal amount.

Trap #3 – Refinancing Too Often

As mentioned at the start of this post I have refinanced 3 times in the 9 years we have had our home.

It can be easy with the internet and a constant bombardment of new financing deals to hunt for the cheapest interest rate every month or two or three.

But be mindful there are costs involved- such as the discharge mortgage fee, the legal fees, admin fees and other bits and bid fees

If you refinance too often the benefits in getting a better interest rate are offset by the constant changing and charging of bank fees.

While I make it a habit to check every year how our home loan is going it’s important to be vigilant but also viable .

Who Did We Refinance with Recently?

While the ink hasn’t yet dried on our legal e-forms yet, we have been unconditionally approved to refinance with our new home loan lender Athena Home Loans .

If you’d like to receive a $250 bonus for signing up, use this referral code during the application process

ATH-82464

Athena will give you $250 and will also give me $250 too it’s a win:win for us both!

What I really enjoyed about their home loan application process was how easy it was to be in control of what I wanted, such as the term. And how it genuinely felt like these guys wanted to help reduce and pay for my loan (wouldn’t every lender?).

They offered the same highly competitive interest rate Ubank were at 2.84%. They provided the flexibility of setting my own term, and payment frequency.

But what I was really impressed with was how they connected to my bank account to fetch the last 6 months of transactions and how they automatically classified them into subcategories.

This made the process of declaring expenditures so much easier than Ubank’s (which was completely manual). Now I understand some people might feel a little uncomfortable with providing a lender direct access to al their accounts, and you can still elect to enter the details manually – you’ll just have to enter these values into subcategories.

Conclusion

Overall I was very impressed with how smooth the application process was with Athena. I sure hope these guys continue to stick around and pass through the rate cuts they have been doing over the last year.

One final aside is that I’ve heard they also pass on a 1 basis point discount for each successive year you remain with them up to a maximum of 5 years (eg. if I stay with them for 5 years my initial interest rate of 2.84% would reduce down to 2.79% if interest rates happen to be at the same rate in 5 years time). It may not sound like much but you can tell they genuinely want to help in reducing your debt and getting the loan paid off quicker!

I don’t receive any kickbacks or anything for this endorsement, but if you’re looking for a good deal check out Athena, and don’t fall into the trap of making your refinancing worse than when you started.